It has been demonstrated time and again that businesses working with experienced accounting professionals can benefit from the strategic financial guidance and compliance support they may provide. Yet these factors alone are often not enough to make the business owner happy. For most small business owners and growing enterprise stakeholders, the lack of proactive advice compounded by slow responses to business requests are the primary reasons for leaving their CPA.

Even if they don’t know how to ask for it, small businesses want proactive attention from their accounting professionals. Small businesses want and need to get information when it matters, and they need help deciphering what the information really means.

It is common for professional accounting firms to simply wait for their clients to provide after-the-fact information from which reports are prepared and delivered long after their relevance has passed. These firms often see no sense of urgency in helping clients address the business issues facing them in real-time.

Business owners attempting to grow a small enterprise from their budding small business especially need the benefit of experienced insight into operational metrics, cash flows and overall business performance. Without this meaningful data and advice delivered in real-time, stakeholders don’t really know what is going on or if they’re on the right path.

Advice on business planning and financial strategies should come to business owners from their accounting professionals, but it often does not. It is interesting that so many firms list business planning and strategy among the services promoted on their websites, yet they just sit back and wait for clients to ask for help.

Regulatory and reporting requirements for businesses are ever-increasing, so it makes some sense that many professional practices continue to focus on taxes and compliance work. Firms may find it challenging enough to keep up with changes to these core services provided. Yet this is why practitioners should take notice and accept that their ability to meet changing market and customer demands is wrapped in their ability to leverage technology to do what people and process can’t do alone.

Information technology is needed to speed up the bookkeeping, accounting and reporting processes, and it takes even more technology to help turn data into relevant and useful information. This is where Mendelson Consulting and Noobeh cloud services can help.

Working with businesses of all sizes and encouraging participation by the accounting professional, Mendelson and Noobeh help businesses implement the technology that facilitates faster collection of information throughout the business and then applying solutions that reflect those numbers in ways that helps users visualize the meaning of the data.

Mendelson and Noobeh help CPAs and accounting professionals remove threats of competition and irrelevance by helping them work closer with and deliver greater value to their small business clients. Applying proven, innovative technologies with improved processing methods and controls leads to better information provided in a timelier manner, which returns to the client as a better result offering greater insight. This is what small businesses want from their CPA, and Mendelson Consulting and Noobeh Cloud Services helps professionals deliver it.

Make sense?

Make sense?

J

Every year-end brings with it not just the holiday spirit, but also the underlying dread felt by small business owners – a creepy and back-of-your-neck hair-raising feeling associated with annual business tax reporting and filing. That old saying about “death and taxes” has a lot of validity to it; sometimes they feel like the same thing to a small business owner. And this is the filing season. Ho ho ho.

Every year-end brings with it not just the holiday spirit, but also the underlying dread felt by small business owners – a creepy and back-of-your-neck hair-raising feeling associated with annual business tax reporting and filing. That old saying about “death and taxes” has a lot of validity to it; sometimes they feel like the same thing to a small business owner. And this is the filing season. Ho ho ho. Make Sense?

Make Sense?

Reporting requirements for business just keep growing, and so do the penalties for doing it wrong. New this year and just in time for the annual reporting season (makes it sound almost fun, huh?) are new forms to file and an increase in penalties for not making an effort to get the information correct and into the hands of the proper recipient. Failure to file by the due date can cost businesses $250 per item, up to $3,000,000 in penalties ($1,000,000 for small businesses). Add to that the warning about intentionally not filing or having an “

Reporting requirements for business just keep growing, and so do the penalties for doing it wrong. New this year and just in time for the annual reporting season (makes it sound almost fun, huh?) are new forms to file and an increase in penalties for not making an effort to get the information correct and into the hands of the proper recipient. Failure to file by the due date can cost businesses $250 per item, up to $3,000,000 in penalties ($1,000,000 for small businesses). Add to that the warning about intentionally not filing or having an “ Make Sense?

Make Sense?

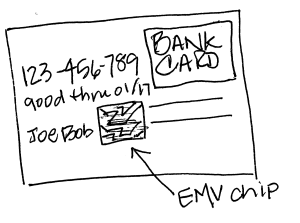

No retailer wants to become the next Target (pun intended). Payment card fraud costs businesses and consumers billions of dollars every year. What’s even more frightening, many of the breaches in the news are the result of innocent participants inadvertently granting access to the bad guys. The Target breach in 2013 exposed the data of 110 million payment cards. Hackers got into the network using perfectly good credentials of the HVAC company. Sometimes password security just isn’t enough, which might bring in to question the security of all those SaaS subscriptions and online shopping sites folks use these days.

No retailer wants to become the next Target (pun intended). Payment card fraud costs businesses and consumers billions of dollars every year. What’s even more frightening, many of the breaches in the news are the result of innocent participants inadvertently granting access to the bad guys. The Target breach in 2013 exposed the data of 110 million payment cards. Hackers got into the network using perfectly good credentials of the HVAC company. Sometimes password security just isn’t enough, which might bring in to question the security of all those SaaS subscriptions and online shopping sites folks use these days.

There is ‘big change a comin’ for retailers, merchants and any business that accepts credit cards for payments, and there are a great many businesses that are completely unprepared for it. The change, what is being referred to as the “

There is ‘big change a comin’ for retailers, merchants and any business that accepts credit cards for payments, and there are a great many businesses that are completely unprepared for it. The change, what is being referred to as the “